Walk into any crypto community and you’ll hear the phrase constantly: “Does this token have utility?” It’s become one of the most repeated questions in the industry — asked in Discord servers, debated on Twitter, and used as a quick litmus test for whether a project is “legit” or just another speculative gamble.

But despite how often the term gets thrown around, a lot of people — including experienced traders — struggle to actually define it clearly. What does “utility” really mean for a token? Why does it matter so much? And how do you evaluate whether a project’s claimed utility is real or just marketing dressed up in technical language?

This guide breaks down token utility from the ground up — what it actually means, the different forms it takes, how to evaluate it critically, and why it’s become one of the central dividing lines between sustainable crypto projects and short-lived speculation.

What Does “Token Utility” Actually Mean?

Token utility refers to the practical use, function, or purpose that a cryptocurrency token serves within its ecosystem, beyond simply being bought, held, or traded for potential profit.

In simpler terms: utility is the answer to the question “what does this token actually do?”

A token with strong utility has a clear, functional role. It might be required to access a service, pay transaction fees, participate in governance decisions, earn rewards for contributing resources, or unlock specific features within a platform. Its value is at least partially tied to genuine demand generated by people who want to use the network or product — not purely by speculators hoping the price goes up.

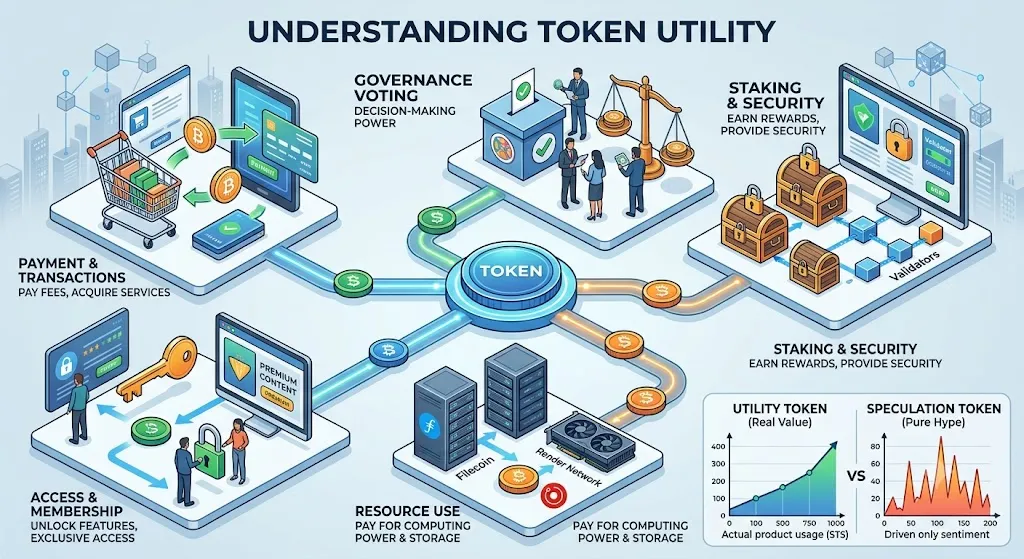

A token without utility — sometimes informally called a “pure speculation token” — exists primarily as a tradeable asset. Its price is driven almost entirely by sentiment, hype, and trading activity, with no underlying functional demand supporting it.

This distinction matters enormously, because it shapes how a token’s value behaves over time, what drives its price, and whether a project has any realistic path toward long-term sustainability.

Why Utility Matters So Much in Crypto

To understand why utility has become such a central concept, it helps to understand what problem it’s actually solving.

The cryptocurrency market is enormous, and a huge percentage of tokens in existence — by some estimates, the vast majority — have no real use case whatsoever. They were created quickly, marketed aggressively, and exist purely as vehicles for speculation. Many of these tokens experience dramatic price spikes followed by total collapse, a pattern that has repeated thousands of times across multiple market cycles.

Utility serves as one of the clearest signals separating projects built to deliver genuine value from projects built primarily to extract value from investors. It’s not a perfect signal — plenty of tokens with genuine utility still fail, and plenty of low-utility tokens have produced enormous short-term gains for traders who timed things well. But over the long run, sustainable token value tends to require some form of real demand beyond pure speculation.

There’s also a structural economic reason utility matters. A token that people need to acquire in order to do something — pay for a service, stake for rewards, participate in governance — creates ongoing buy pressure tied to actual usage of the network. As adoption grows, demand for the token can grow alongside it. A token with no functional use case has no such mechanism. Its price depends entirely on more buyers continuing to enter the market with the expectation of selling to someone else later — a dynamic that becomes unstable once new buyer interest slows down.

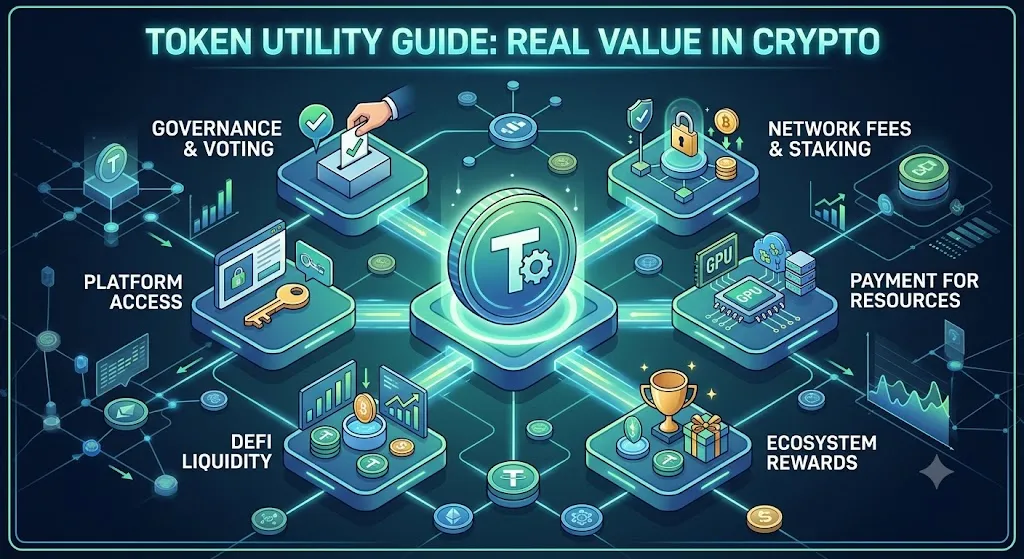

The Main Categories of Token Utility

Token utility isn’t a single thing — it takes many different forms depending on the type of project and what problem it’s trying to solve. Understanding these categories will help you evaluate any specific token more precisely.

Payment and Transaction Utility

This is the most straightforward form of utility: the token is used as a medium of exchange for goods, services, or transaction fees within its ecosystem.

Bitcoin’s original use case falls into this category — a peer-to-peer digital currency that can be used to pay for things directly. Ethereum’s ETH token is used to pay “gas fees,” the transaction costs required to execute operations on the Ethereum network, including smart contract interactions, token transfers, and decentralized application usage.

Many Layer 1 blockchains follow this same model: their native token is required to pay for any activity that happens on the network. As usage of the network grows, demand for the token to pay these fees grows correspondingly.

Governance Utility

Many decentralized projects are governed not by a centralized company but by their token holders, through a structure often called a DAO (Decentralized Autonomous Organization). In these systems, holding the project’s token gives you voting rights on key decisions — protocol upgrades, fee structures, treasury allocation, partnership approvals, and other major changes.

This is sometimes called a “governance token.” Uniswap’s UNI token, for example, gives holders voting power over changes to the Uniswap protocol. MakerDAO’s MKR token allows holders to vote on parameters affecting the DAI stablecoin system.

Governance utility ties a token’s value partly to the value of having a say in how an important, valuable protocol is run. The strength of this utility depends heavily on how much real decision-making power token holders actually have, and how valuable the underlying protocol is.

Staking and Network Security Utility

In many blockchain networks that use a Proof of Stake consensus mechanism, the native token must be staked — locked up as collateral — in order to participate in validating transactions and securing the network. Validators who behave honestly earn staking rewards. Validators who act maliciously can have their staked tokens slashed (partially or fully confiscated) as a penalty.

This creates a direct functional requirement for the token: you need to hold and stake it in order to participate in securing the network and earning rewards. Ethereum (after its transition to Proof of Stake), Solana, Cardano, and many other major blockchains rely on this model.

This form of utility ties token demand directly to network security — the more value secured by the network, the more economic incentive there is for token holders to stake and participate, which in turn increases demand for acquiring and holding the token.

Access and Membership Utility

Some tokens function as a key that unlocks access to a specific product, service, platform, or community. Holding a certain amount of the token might be required to use premium features of an application, access exclusive content, join a private community, or participate in specific platform functions.

This model has become especially common in combination with NFT projects, where token or NFT ownership grants access to gated Discord channels, special events, voting rights on community decisions, or early access to future products.

The strength of this utility depends entirely on how valuable the access actually is. A token that grants access to a thriving, valuable ecosystem has real utility. A token that grants access to a Discord server with declining engagement has very little.

Utility in Decentralized Finance (DeFi)

DeFi protocols — decentralized lending platforms, exchanges, yield aggregators, and similar applications — often have native tokens with multiple layered utility functions specific to how the protocol operates.

This might include: collateral that can be deposited to borrow other assets, liquidity provider rewards for supplying tokens to a trading pool, fee discounts for users who hold or stake the token, or a share of protocol revenue distributed to token holders.

Some of the most established DeFi protocols have built token models where holders receive a portion of the fees generated by the protocol’s activity — directly tying token value to the platform’s actual usage and revenue, similar to how a dividend-paying stock ties value to company earnings.

Computational and Resource Utility

Certain blockchain projects build decentralized marketplaces for real-world resources — computing power, data storage, bandwidth, or other infrastructure — and use their native token as the payment mechanism within that marketplace.

Filecoin, for example, uses its FIL token to pay for decentralized data storage, with storage providers earning FIL for hosting data on the network. Render Network’s RENDER token pays for decentralized GPU rendering services. These tokens have utility directly tied to genuine, measurable demand for a real-world resource.

This category has grown significantly with the rise of AI-related crypto projects, many of which use tokens to facilitate marketplaces for computing power needed to train and run AI models.

Burn Mechanisms and Deflationary Utility

Some projects build mechanisms where tokens are permanently removed from circulation (“burned”) based on network activity — for example, a portion of every transaction fee might be burned rather than paid to validators. This reduces total token supply over time, which can support price appreciation if demand remains constant or grows.

While burning isn’t utility in the same functional sense as the categories above, it’s often paired with genuine utility mechanisms to create additional scarcity pressure tied to actual network usage. Ethereum implemented a fee-burning mechanism (EIP-1559) that ties ETH supply reduction directly to network activity.

Real Utility vs. Manufactured Utility: How to Tell the Difference

Here’s where things get genuinely important for anyone trying to evaluate crypto projects: not all claimed utility is created equal. Many projects describe elaborate “utility” for their token that, on closer examination, is either unnecessary, artificially imposed, or simply doesn’t hold up.

Ask: Would this work just as well — or better — without the token?

This is the single most useful question for evaluating utility claims. If a project’s stated use case could be accomplished just as effectively using an existing established cryptocurrency like ETH, USDC, or SOL, or even without blockchain at all, then the “utility” being described may be artificially manufactured to justify the token’s existence rather than representing a genuine functional need.

Some projects, for example, require their native token for payments specifically because the team wants the token to have built-in demand — not because there’s any genuine technical or economic reason that token, specifically, needs to exist. This is sometimes called a forced utility model, and it tends to produce friction for users (who now need to acquire a specific, often illiquid token just to use a service) without producing real long-term value.

Ask: Does usage of the product actually require ongoing token demand?

Strong utility typically creates a repeated, sustained reason for people to acquire the token, tied to actual usage of the underlying product or network. Weak or manufactured utility often involves a one-time or rarely-repeated use case, which doesn’t generate sustained buy pressure.

Ask: Is the utility live and functioning, or only theoretical?

Many projects describe utility that exists only on a roadmap or in a whitepaper, with no functioning product behind it. A governance system that hasn’t launched yet provides no actual governance utility today, regardless of how it’s described in marketing materials. Always distinguish between utility that exists right now, in a working product, and utility that’s promised for some future date.

Ask: Does the utility scale with adoption, or is it capped?

The most powerful utility models scale naturally as a network grows — more users means more transactions, more fees paid, more staking demand, and so on. Weaker models might have utility that doesn’t meaningfully increase even if user numbers grow significantly, limiting the connection between project success and token value.

Ask: Who actually benefits from the utility?

Sometimes a “utility” mechanism primarily benefits the project’s founding team or early investors rather than creating genuine value for ordinary token holders or users. A staking mechanism that pays disproportionate rewards to whales, or a governance system effectively controlled by a small number of large holders, has much weaker genuine utility than the marketing suggests.

Utility Tokens vs. Security Tokens: A Critical Legal Distinction

The concept of “utility” carries significant legal weight in the cryptocurrency industry, particularly in the United States, where it intersects directly with securities law.

Regulators, most notably the U.S. Securities and Exchange Commission, have spent years working through how to classify different types of crypto tokens. One of the central legal questions is whether a token qualifies as a security — a regulated financial instrument subject to extensive disclosure and registration requirements — or as something else, such as a utility token that falls outside securities regulation.

The most commonly referenced legal test for this distinction is the Howey Test, derived from a 1946 U.S. Supreme Court case, which asks whether an investment involves: money invested in a common enterprise, with an expectation of profit, derived primarily from the efforts of others.

Projects have often argued that tokens with genuine functional utility — tokens you need to actually use a product or service — should not be classified as securities, since buyers are acquiring them to use a product rather than purely as a passive investment expecting profit from the issuer’s efforts.

This is part of why “utility” became such a heavily emphasized concept industry-wide: many projects explicitly designed and marketed their tokens as utility tokens specifically to argue they fall outside securities regulation. Regulators have pushed back on this framing in numerous cases, arguing that a token marketed primarily on the basis of price appreciation potential — regardless of whether some functional utility also exists — may still meet the legal definition of a security.

This is genuinely complicated legal territory, and it continues to evolve through ongoing regulatory actions and court cases. It’s worth understanding as context for why projects emphasize utility so heavily in their communications — there are real legal incentives at play beyond purely making the case for the token’s economic value.

How to Evaluate Token Utility: A Practical Checklist

When researching any crypto project, here’s a structured approach to evaluating its claimed utility:

Read the tokenomics section of the whitepaper carefully, not just the marketing summary. Identify exactly what mechanisms require the token and exactly how those mechanisms function.

Check whether the utility is live in a working product today, or only planned for the future. Visit the actual platform if possible and verify the described functionality works as claimed.

Look at on-chain data to see whether the described utility is actually being used. If a token is supposedly required for staking, check how many tokens are actually staked. If it’s supposedly used for governance, check how many holders actually participate in votes. Low actual usage despite an impressive-sounding utility description is a red flag.

Consider whether the utility could be accomplished without this specific token. If yes, ask why the project chose to require its own token rather than using an established alternative — and whether the answer is a genuine technical reason or simply a tokenomics decision designed to create artificial demand.

Examine how utility-related rewards are distributed. Check whether rewards from staking, fee-sharing, or other utility mechanisms are concentrated among a small number of large holders, which would undermine the broader value proposition for smaller investors.

Assess whether the utility scales with adoption. Project forward: if this network had ten times the current number of users, would token demand meaningfully increase as a result? If the answer is unclear or no, the utility may be weaker than it initially appears.

Research the project’s regulatory positioning and any past or ongoing regulatory scrutiny. This can offer insight into whether independent observers — including regulators with strong investigative resources — view the project’s utility claims as substantive or as a thin justification for what is functionally a speculative investment vehicle.

Examples of Tokens Widely Regarded as Having Strong Utility

While no token is beyond criticism, certain projects are commonly cited as having relatively well-established, functioning utility models:

Ethereum (ETH) is required to pay gas fees for any transaction or smart contract interaction on the network, and is also used for staking to secure the network under its Proof of Stake system. Demand for ETH is directly tied to the immense and growing volume of activity on the Ethereum network, including DeFi, NFTs, and a vast ecosystem of decentralized applications.

Chainlink (LINK) is used to pay node operators who provide reliable, decentralized data feeds (oracles) to smart contracts across many different blockchains. As more DeFi and other smart contract applications depend on accurate external data, demand for Chainlink’s oracle services — and the LINK token used to access them — grows correspondingly.

Filecoin (FIL) is required as payment for decentralized data storage services, with storage providers earning FIL for hosting data and users spending FIL to store it. This ties token demand directly to actual storage capacity usage on the network.

Maker (MKR) governs the Maker Protocol, which issues the DAI stablecoin. MKR holders vote on crucial risk parameters that determine the stability and solvency of one of the largest decentralized stablecoins in existence — a genuinely important governance function with real consequences.

A Word of Caution: Utility Doesn’t Guarantee Investment Success

It’s worth being direct about something many crypto educational resources gloss over: having genuine utility does not guarantee that a token will be a good investment, nor does it protect against price decline.

Plenty of tokens with legitimate, functioning utility have still seen dramatic price drops due to broader market conditions, increased competition, declining usage, poor tokenomics design (such as excessive token emissions diluting holders), or simply market sentiment shifting away from a particular sector.

Utility is best understood as one important factor among several that should inform your evaluation of a crypto project — not a guarantee of price performance. A token can have excellent, genuine utility and still be a poor investment at a given price point if that utility is already fully reflected in (or even exceeded by) the current valuation. Conversely, evaluating utility is about assessing the fundamental health and sustainability of a project, which is different from, though related to, assessing whether its current price represents a good buying opportunity.

The most sophisticated crypto investors tend to treat utility analysis as part of a broader fundamental analysis process — alongside tokenomics, team evaluation, competitive positioning, and market timing — rather than as a standalone signal to buy or sell.

Final Thoughts

Token utility is one of the most important concepts for understanding the difference between crypto projects built to create lasting value and those built primarily to generate short-term speculative interest. At its core, it’s a simple question with significant implications: what does this token actually do, and does that function generate real, sustained demand?

The honest reality is that most tokens in the cryptocurrency market today have weak or nonexistent genuine utility. They exist primarily as speculative trading vehicles, regardless of how their utility is described in marketing materials. Recognizing this — and developing the analytical skills to distinguish real utility from manufactured utility — is one of the most valuable capabilities you can build as a participant in this market.

That said, genuine utility absolutely does exist, and the projects that have built real, functioning ecosystems around their tokens represent some of the most significant developments in the entire blockchain industry. Understanding how to identify and evaluate this utility — critically, skeptically, and with attention to actual on-chain evidence rather than whitepaper promises — is foundational knowledge for anyone serious about navigating this space.

The next time you see a project claim its token has “strong utility,” you now have a framework for actually testing that claim rather than simply taking it at face value. That skill alone will put you ahead of a large percentage of market participants.

Disclaimer: This article is for educational and informational purposes only and does not constitute financial, investment, or legal advice. Cryptocurrency investments carry significant risk, including the potential loss of capital. Always conduct your own research and consult a qualified financial advisor before making investment decisions.

Frequently Asked Questions

Token utility refers to the practical purpose or function of a cryptocurrency token within a blockchain ecosystem, such as paying fees, staking, governance, or accessing services.

Strong token utility can create real demand for a cryptocurrency, support long-term adoption, and help distinguish legitimate projects from purely speculative ones.

Common examples include paying network transaction fees, participating in governance votes, staking to secure a blockchain, accessing platform features, and earning rewards.

No. While utility is an important factor, it does not guarantee price appreciation. Market conditions, competition, tokenomics, and adoption also influence a token’s value.

Look for a real-world use case, an active product or ecosystem, sustainable demand, transparent tokenomics, and evidence that the token is genuinely needed rather than included only for marketing purposes.

Leave a Reply